Crooks who make a living via identity theft schemes, dating scams and other con games often run into trouble when presented with a phone-based challenge that requires them to demonstrate mastery of a language they don’t speak fluently. Enter the criminal call center, which allows scammers to outsource those calls to multi-lingual men and women who can be hired to close the deal.

Some of these call centers are Web-based, allowing customers to upload information about their targets to a service that initiates the call to a bank, credit provider, shipping company or dating scam victim (for more on the role played by call centers in dating schemes, see last week’s story, Fraudsters Automate Russian Dating Scams). Other call centers require customers to supply information about the target and the needed service via Jabber instant message. This post focuses on Web-based call services.

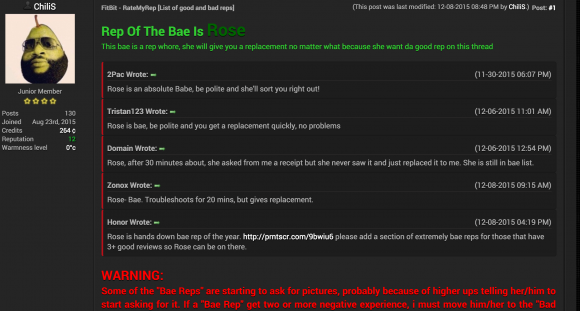

In the call service pictured below, we can see one user ordering a $250 radio-controlled toy Ford Mustang as a gift for someone’s kid for the holidays. The customer of the call service specifies the American Express card account to be used for the transaction, and requests that the order be expedited to a reshipping mule who will forward the goods to Russia. The status of the transaction indicates that this particular order was successfully placed on Jan. 7, 2016.

A customer of this crooked call center is ordering a holiday gift for someone’s kid.

One of the cybercrime underground’s oldest call center services — CallMeBaby — serves a variety of swindles but specializes in helping criminals cash out dating scams. It charges $10 for each call in English, and $12 for calls in German, French, Italian, Spanish, Portuguese and Polish. Here’s an ad for the four-year-old service, which features an illustration of a blonde woman chatting with President Obama:

An underground ad for a call service run by a cybercrook who uses the nickname “Sparta.”

CallMeBaby advertises the availability of a male and female to impersonate anyone in the above-supported languages, and operates between the hours of 17:00 to 03:00 Moscow time (business hours in America). Continue reading

Absolutely none of this would be possible without you, Dear Reader. You have supported, encouraged and inspired me in too many ways to count these past years. The community that’s sprung up around here has been a joy to watch, and essential to the site’s success. Thank you!

Absolutely none of this would be possible without you, Dear Reader. You have supported, encouraged and inspired me in too many ways to count these past years. The community that’s sprung up around here has been a joy to watch, and essential to the site’s success. Thank you! The new Flash version, v. 20.0.0.267 for most Mac and Windows users, includes a fix for a vulnerability (CVE-2015-8651) that Adobe

The new Flash version, v. 20.0.0.267 for most Mac and Windows users, includes a fix for a vulnerability (CVE-2015-8651) that Adobe

Hyatt’s

Hyatt’s  New authentication methods now offered by Yahoo! and to a beta group of Google users let customers log in just by supplying their email address, and then responding to a notification sent to their mobile device.

New authentication methods now offered by Yahoo! and to a beta group of Google users let customers log in just by supplying their email address, and then responding to a notification sent to their mobile device.

The FTC sued Oracle over years of failing to remove older, more vulnerable versions of Java SE when consumers updated their systems to the newest Java software. Java is installed on more than 850 million computers, but only recently (in Aug. 2014) did the company change its updater software to reliably remove older versions of Java during the installation process.

The FTC sued Oracle over years of failing to remove older, more vulnerable versions of Java SE when consumers updated their systems to the newest Java software. Java is installed on more than 850 million computers, but only recently (in Aug. 2014) did the company change its updater software to reliably remove older versions of Java during the installation process. Mountain View, Calif. based Gyft lets customers buy and use gift cards entirely from their mobile devices. Acting on a tip from a trusted source in the cybercrime underground who reported that a cache of account data on Gyft customers was on offer for the right bidder, KrebsOnSecurity contacted Gyft to share intelligence and to request comment.

Mountain View, Calif. based Gyft lets customers buy and use gift cards entirely from their mobile devices. Acting on a tip from a trusted source in the cybercrime underground who reported that a cache of account data on Gyft customers was on offer for the right bidder, KrebsOnSecurity contacted Gyft to share intelligence and to request comment.