Many news sites and blogs are reporting that the data stolen last month from 37 million users of AshleyMadison.com — a site that facilitates cheating and extramarital affairs — has finally been posted online for the world to see. In the past 48 hours, several huge dumps of data claiming to be the actual AshleyMadison database have turned up online. But there are precious few details in them that would allow one to verify these claims, and the company itself says it so far sees no indication that the files are legitimate.

Update, 11:52 p.m. ET: I’ve now spoken with three vouched sources who all have reported finding their information and last four digits of their credit card numbers in the leaked database. Also, it occurs to me that it’s been almost exactly 30 days since the original hack. Finally, all of the accounts created at Bugmenot.com for Ashleymadison.com prior to the original breach appear to be in the leaked data set as well. I’m sure there are millions of AshleyMadison users who wish it weren’t so, but there is every indication this dump is the real deal.

Original story:

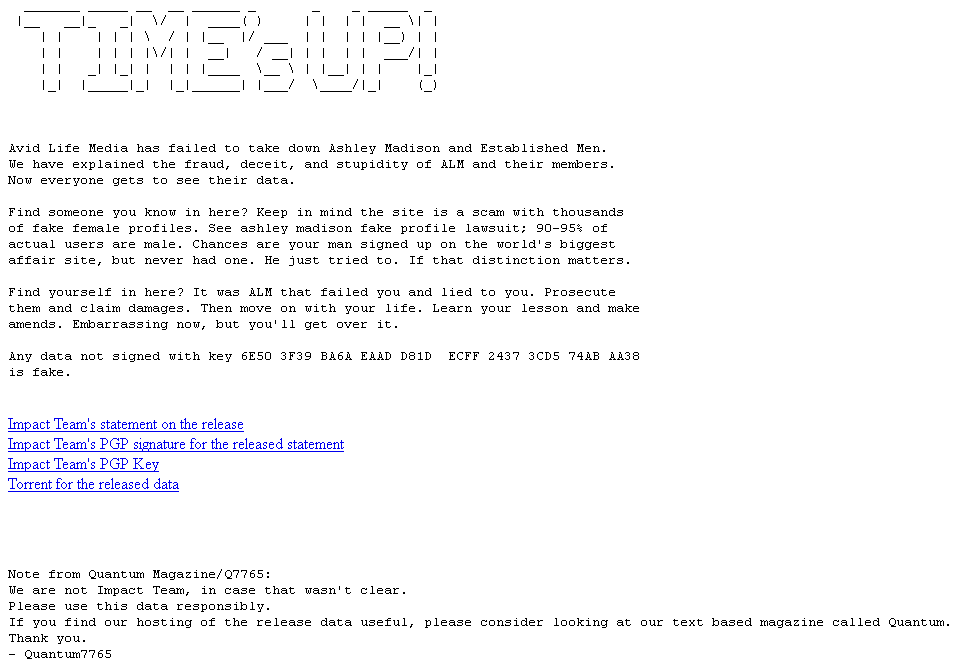

A huge trove of data nearly 10 gigabytes in size was dumped onto the Deep Web and onto various Torrent file-sharing services over the past 48 hours. According to a story at Wired.com, included in the files are names, addresses and phone numbers apparently attached to AshleyMadison member profiles, along with credit card data and transaction information. Links to the files were preceded by a text file message titled “Time’s Up” (see screenshot below).

The message left by the latest group claiming to have leaked the hacked AshleyMadison.com database.

From taking in much of the media coverage of this leak so far — for example, from the aforementioned Wired piece or from the story at security blogger Graham Cluley’s site — readers would most likely conclude that this latest collection of leaked data is legitimate. But after an interview this evening with Raja Bhatia — AshleyMadison’s original founding chief technology officer — I came away with a different perspective.

Bhatia said he is working with an international team of roughly a dozen investigators who are toiling seven days a week, 24-hours a day just to keep up with all of the fake data dumps claiming to be the stolen AshleyMadison database that was referenced by the original hackers on July 19. Bhatia said his team sees no signs that this latest dump is legitimate.

“On a daily basis, we’re seeing 30 to 80 different claimed dumps come online, and most of these dumps are entirely fake and being used by other organizations to capture the attention that’s been built up through this release,” Bhatia said. “In total we’ve looked at over 100GB of data that’s been put out there. For example, I just now got a text message from our analysis team in Israel saying that the last dump they saw was 15 gigabytes. We’re still going through that, but for the most part it looks illegitimate and many of the files aren’t even readable.”

The former AshleyMadison CTO, who’s been consulting for the company ever since news of the hack broke last month, said many of the fake data dumps the company has examined to date include some or all of the files from the original July 19 release. But the rest of the information, he said, is always a mix of data taken from other hacked sources — not AshleyMadison.com.

“The overwhelming amount of data released in the last three weeks is fake data,” he said. “But we’re taking every release seriously and looking at each piece of data and trying to analyze the source and the veracity of the data.”

Bhatia said the format of the fake leaks has been changing constantly over the last few weeks.

“Originally, it was being posted through Imgur.com and Pastebin.com, and now we’re seeing files going out over torrents, the Dark Web, and TOR-based URLs,” he said.

To help locate new troves of data claiming to be the files stolen from AshleyMadison, the company’s forensics team has been using a tool that Netflix released last year called Scumblr, which scours high-profile sites for specific terms and data.

“For the most part, we can quickly verify that it’s not our data or it’s fake data, but we are taking each release seriously,” Bhatia said. “Scumbler helps accelerate the time it takes for us to detect new pieces of data that are being released. For the most part, we’re finding the majority of it is fake. There are some things that have data from the original release, but other than that, what we’re seeing is other generic files that have been introduced, fake SQL files.” Continue reading