KrebsOnSecurity turns 13 years old today. That’s a crazy long time for an independent media outlet these days, but then again I’m bound to keep doing this as long as they keep letting me. Heck, I’ve been doing this so long I briefly forgot which birthday this was!

Thanks to your readership and support, I was able to spend more time in 2022 on some deep, meaty investigative stories — the really satisfying kind with the potential to effect positive change. Some of that work is highlighted in the 2022 Year in Review review below.

Until recently, I was fairly active on Twitter, regularly tweeting to more than 350,000 followers about important security news and stories here. For a variety of reasons, I will no longer be sharing these updates on Twitter. I seem to be doing most of that activity now on Mastodon, which appears to have absorbed most of the infosec refugees from Twitter, and in any case is proving to be a far more useful, civil and constructive place to post such things. I will also continue to post on LinkedIn about new stories in 2023.

Here’s a look at some of the more notable cybercrime stories from the past year, as covered by KrebsOnSecurity and elsewhere. Several strong themes emerged from 2022’s crop of breaches, including the targeting or impersonating of employees to gain access to internal company tools; multiple intrusions at the same victim company; and less-than-forthcoming statements from victim firms about what actually transpired.

JANUARY

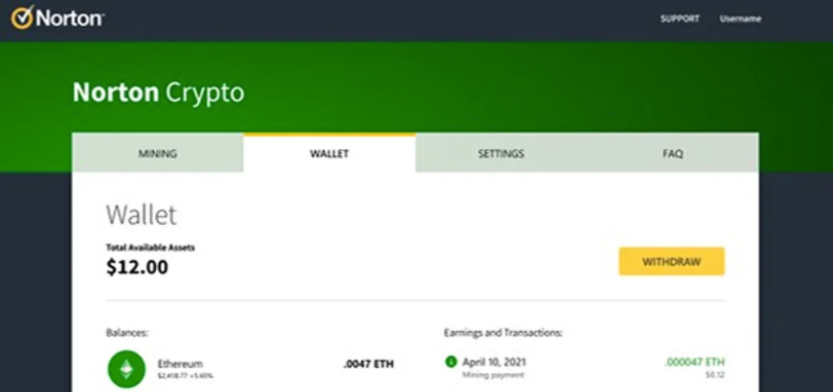

You just knew 2022 was going to be The Year of Crypto Grift when two of the world’s most popular antivirus makers — Norton and Avira — kicked things off by installing cryptocurrency mining programs on customer computers. This bold about-face dumbfounded many longtime Norton users because antivirus firms had spent years broadly classifying all cryptomining programs as malware.

Suddenly, hundreds of millions of users — many of them old enough to have bought antivirus from Peter Norton himself back in the day — were being encouraged to start caring about and investing in crypto. Big Yellow and Avira weren’t the only established brands cashing in on crypto hype as a way to appeal to a broader audience: The venerable electronics retailer RadioShack wasted no time in announcing plans to launch a cryptocurrency exchange.

By the second week of January, Russia had amassed more than 100,000 troops along its southern border with Ukraine. The Kremlin breaks with all tradition and announces that — at the request of the United States — it has arrested 14 people suspected of working for REvil, one of the more ruthless and profitable Russian ransomware groups.

Security and Russia experts dismiss the low-level arrests as a kind of “ransomware diplomacy,” a signal to the United States that if it doesn’t enact severe sanctions against Russia for invading Ukraine, Russia will continue to cooperate on ransomware investigations.

The Jan. 19th story IRS Will Soon Require Selfies For Online Access goes immediately viral for pointing out something that apparently nobody has noticed on the U.S. Internal Revenue Service website for months: Anyone seeking to create an account to view their tax records online would soon be required to provide biometric data to a private company in Virginia — ID.me.

Facing a backlash from lawmakers and the public, the IRS soon reverses course, saying video selfies will be optional and that any biometric data collected will be destroyed after verification.

FEBRUARY

Super Bowl Sunday watchers are treated to no fewer than a half-dozen commercials for cryptocurrency investing. Matt Damon sells his soul to Crypto.com, telling viewers that “fortune favors the brave” — basically, “only cowards would fail to buy cryptocurrency at this point.” Meanwhile, Crypto.com is trying to put space between it and recent headlines that a breach led to $30 million being stolen from hundreds of customer accounts. A single bitcoin is trading at around $45,000.

Larry David, the comedian who brought us years of awkward hilarity with hits like Seinfeld and Curb Your Enthusiasm, plays the part of the “doofus, crypto skeptic” in a lengthy Super Bowl ad for FTX, a cryptocurrency exchange then valued at over $20 billion that is pitched as a “safe and easy way to get into crypto.” [Last month, FTX imploded and filed for bankruptcy; the company’s founder now faces civil and criminal charges from three different U.S. agencies].

On Feb. 24, Russia invades Ukraine, and fault lines quickly begin to appear in the cybercrime underground. Cybercriminal syndicates that previously straddled Russia and Ukraine with ease are forced to reevaluate many comrades who are suddenly working for The Other Side.

Many cybercriminals who operated with impunity from Russia and Ukraine prior to the war chose to flee those countries following the invasion, presenting international law enforcement agencies with rare opportunities to catch most-wanted cybercrooks. One of those is Mark Sokolovsky, a 26-year-old Ukrainian man who operated the popular “Raccoon” malware-as-a-service offering; Sokolovsky was busted in March after fleeing Ukraine’s mandatory military service orders.

Also nabbed on the lam is Vyacheslav “Tank” Penchukov, a senior Ukrainian member of a transnational cybercrime group that stole tens of millions of dollars over nearly a decade from countless hacked businesses. Penchukov was arrested after leaving Ukraine to meet up with his wife in Switzerland.

Tank, seen here performing as a DJ in Ukraine in an undated photo from social media.

Ransomware group Conti chimes in shortly after the invasion, vowing to attack anyone who tries to stand in Mother Russia’s way. Within hours of that declaration several years worth of internal chat logs stolen from Conti were leaked online. The candid employee conversations provide a rare glimpse into the challenges of running a sprawling criminal enterprise with more than 100 salaried employees. The records also reveal how Conti dealt with its own internal breaches and attacks from private security firms and foreign governments.

Faced with an increasing brain drain of smart people fleeing the country, Russia floats a new strategy to address a worsening shortage of qualified information technology experts: Forcing tech-savvy people within the nation’s prison population to perform low-cost IT work for domestic companies.

Chipmaker NVIDIA says a cyberattack led to theft of information on more than 71,000 employees. Credit for that intrusion is quickly claimed by LAPSUS$, a group of 14-18 year-old cyber hooligans mostly from the United Kingdom who specialized in low-tech but highly successful methods of breaking into companies: Targeting employees directly over their mobile phones.

LAPSUS$ soon employs these skills to siphon source code and other data from some of the world’s biggest technology firms, including Microsoft, Okta, Samsung, T-Mobile and Uber, among many others. Continue reading

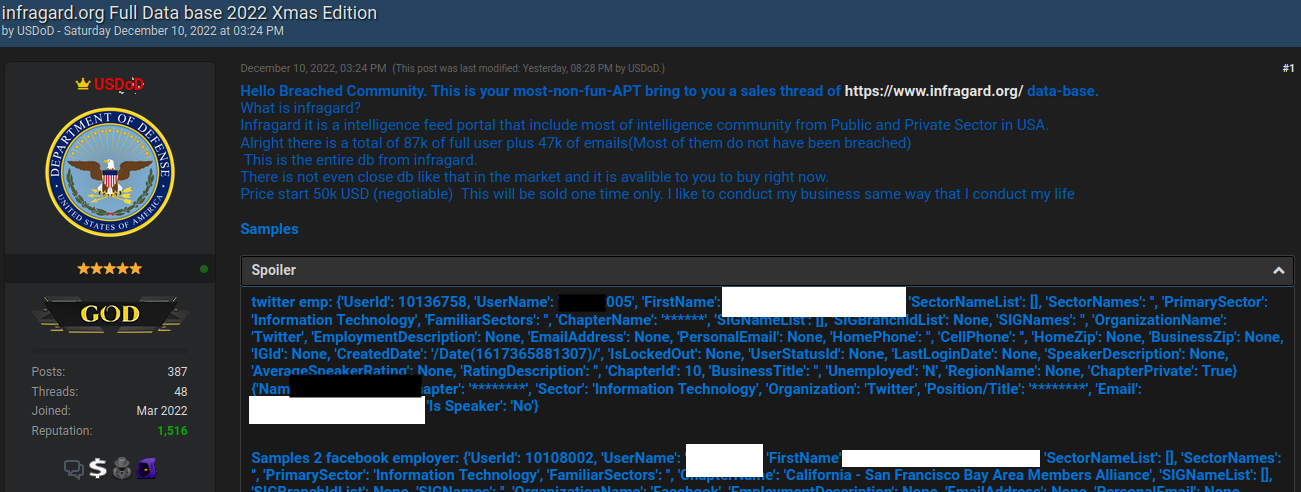

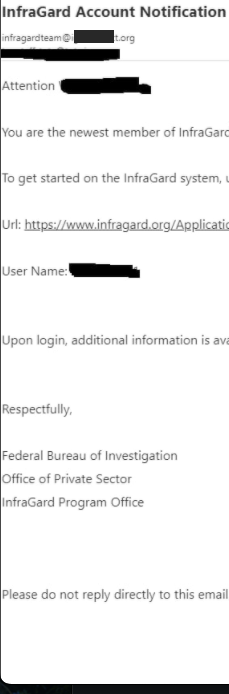

But USDoD said that in early December, their email address in the name of the CEO received a reply saying the application had been approved (see redacted screenshot to the right). While the FBI’s InfraGard system requires multi-factor authentication by default, users can choose between receiving a one-time code via SMS or email.

But USDoD said that in early December, their email address in the name of the CEO received a reply saying the application had been approved (see redacted screenshot to the right). While the FBI’s InfraGard system requires multi-factor authentication by default, users can choose between receiving a one-time code via SMS or email.