In April 2013, I received via U.S. mail more than a gram of pure heroin as part of a scheme to get me arrested for drug possession. But the plan failed and the Ukrainian mastermind behind it soon after was imprisoned for unrelated cybercrime offenses. That individual recently gave his first interview since finishing his jail time here in the states, and he’s shared some select (if often abrasive and coarse) details on how he got into cybercrime and why. Below are a few translated excerpts.

When I first encountered now-31-year-old Sergei “Fly,” “Flycracker,” “MUXACC” Vovnenko in 2013, he was the administrator of the fraud forum “thecc[dot]bz,” an exclusive and closely guarded Russian language board dedicated to financial fraud and identity theft.

Many of the heavy-hitters from other fraud forums had a presence on Fly’s forum, and collectively the group financed and ran a soup-to-nuts network for turning hacked credit card data into mounds of cash.

Vovnenko first came onto my radar after his alter ego Fly published a blog entry that led with an image of my bloodied, severed head and included my credit report, copies of identification documents, pictures of our front door, information about family members, and so on. Fly had invited all of his cybercriminal friends to ruin my financial identity and that of my family.

Somewhat curious about what might have precipitated this outburst, I was secretly given access to Fly’s cybercrime forum and learned he’d freshly hatched a plot to have heroin sent to my home. The plan was to have one of his forum lackeys spoof a call from one of my neighbors to the police when the drugs arrived, complaining that drugs were being delivered to our house and being sold out of our home by Yours Truly.

Thankfully, someone on Fly’s forum also posted a link to the tracking number for the drug shipment. Before the smack arrived, I had a police officer come out and take a report. After the heroin showed up, I gave the drugs to the local police and wrote about the experience in Mail From the Velvet Cybercrime Underground.

Angry that I’d foiled the plan to have me arrested for being a smack dealer, Fly or someone on his forum had a local florist send a gaudy floral arrangement in the shape of a giant cross to my home, complete with a menacing message that addressed my wife and was signed, “Velvet Crabs.”

The floral arrangement that Fly or one of his forum lackeys had delivered to my home in Virginia.

Vovnenko was arrested in Italy in the summer of 2014 on identity theft and botnet charges, and spent some 15 months in arguably Italy’s worst prison contesting his extradition to the United States. Those efforts failed, and he soon pleaded guilty to aggravated identity theft and wire fraud, and spent several years bouncing around America’s prison system.

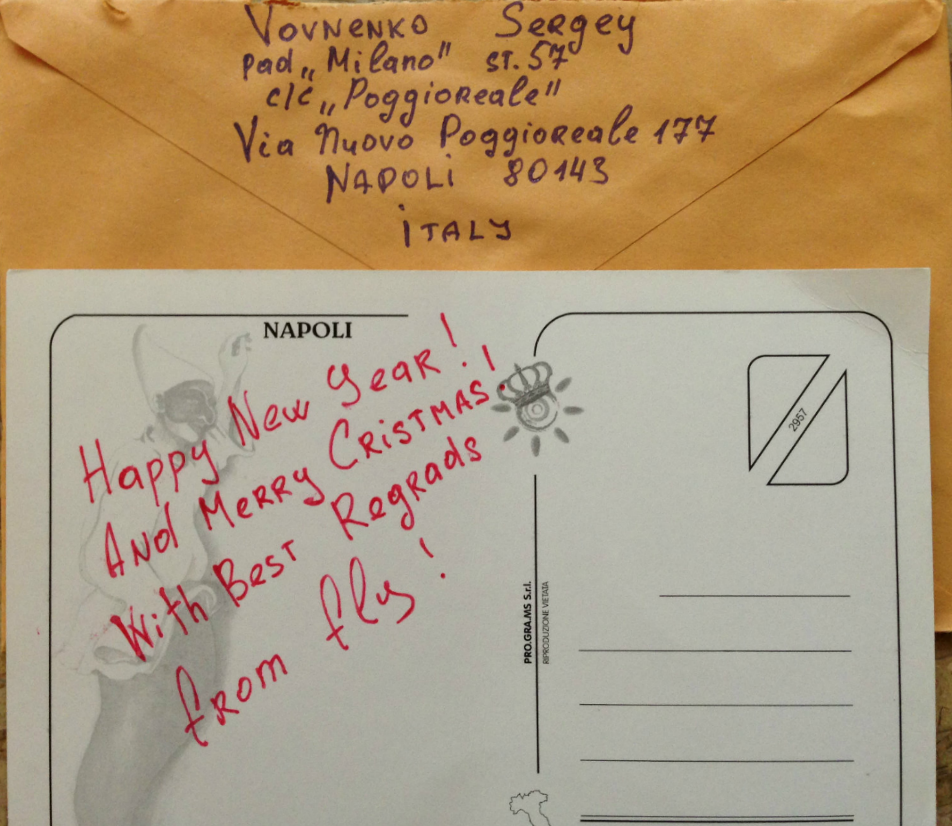

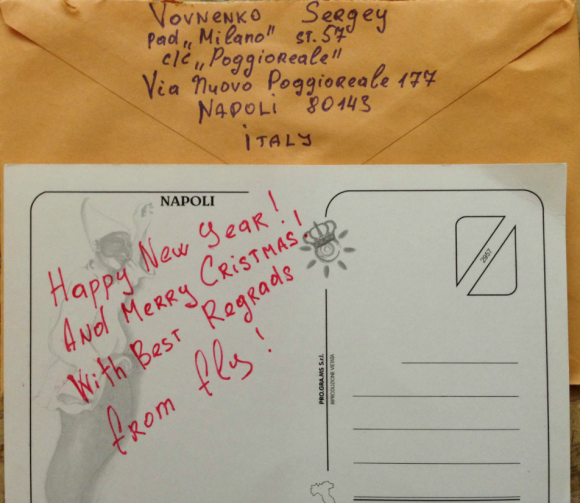

Although Vovnenko sent me a total of three letters from prison in Naples (a hand-written apology letter and two friendly postcards), he never responded to my requests to meet him following his trial and conviction on cybercrime charges in the United States. I suppose that is fair: To my everlasting dismay, I never responded to his Italian dispatches (the first I asked to be professionally analyzed and translated before I would touch it).

Seasons greetings from my pen pal, Flycracker.

After serving his 41 month sentence in the U.S., Vovnenko was deported, although it’s unclear where he currently resides (the interview excerpted here suggests he’s back in Italy, but Fly doesn’t exactly confirm that).

In an interview published on the Russian-language security blog Krober.biz, Vovnenko said he began stealing early in life, and by 13 was already getting picked up for petty robberies and thefts.

A translated English version of the interview was produced and shared with KrebsOnSecurity by analysts at New York City-based cyber intelligence firm Flashpoint. Continue reading

Two of the bugs quashed in this month’s patch batch (

Two of the bugs quashed in this month’s patch batch (

{kind=link}