For many years and until quite recently, credit card data stolen from online merchants has been worth far less in the cybercrime underground than cards pilfered from hacked brick-and-mortar stores. But new data suggests that over the past year, the economics of supply-and-demand have helped to double the average price fetched by card-not-present data, meaning cybercrooks now have far more incentive than ever to target e-commerce stores.

Traditionally, the average price for card data nabbed from online retailers — referred to in the underground as “CVVs” — has ranged somewhere between $2 and $8 per account. CVVs are are almost exclusively purchased by criminals looking to make unauthorized purchases at online stores, a form of thievery known as “card not present” fraud.

In contrast, the value of “dumps” — hacker slang for card data swiped from compromised retail stores, hotels and restaurants with the help of malware installed on point-of-sale systems — has long hovered around $15-$20 per card. Dumps allow street thieves to create physical clones of debit and credit cards, which are then used to perpetrate so-called “card present” fraud at brick and mortar stores.

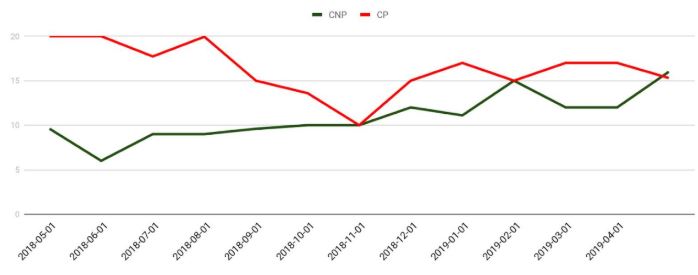

But according to Gemini Advisory, a New York-based company that works with financial institutions to monitor dozens of underground markets trafficking in both types of data, over the past year the demand for CVVs has far outstripped supply, bringing prices for both CVVs and dumps roughly in line with each other.

Median price of card not present (CNP) vs. card-present (CP) over the past year. Image: Gemini

Stas Alforov, director of research and development at Gemini, says his company is currently monitoring most underground stores that peddle stolen card data — including such heavy hitters as Joker’s Stash, Trump’s Dumps, and BriansDump.

Contrary to popular belief, when these shops sell a CVV or dump, that record is then removed from the inventory of items for sale, allowing companies that track such activity to determine roughly how many new cards are put up for sale and how many have sold. Underground markets that do otherwise quickly earn a reputation among criminals for selling unreliable card data and are soon forced out of business.

“We can see in pretty much real-time what’s being sold and which marketplaces are the most active or have the highest number of records and where the bad guys shop the most,” Alforov said. “The biggest trend we’ve seen recently is there appears to be a much greater demand than there is supply of card not present data being uploaded to these markets.”

Alforov said dumps are still way ahead in terms of the overall number of compromised records for sale. For example, over the past year Gemini has seen some 66 million new dumps show up on underground markets, and roughly half as many CVVs.

“The demand for card not present data remains strong while the supply is not as great as the bad guys need it to be, which means prices have been steadily going up,” Alforov said. “A lot of the bad guys who used to do card present fraud are now shifting to card-not-present fraud.”

One likely reason for that shift is the United States is the last of the G20 nations to make the transition to more secure chip-based payment cards, which is slowly making it more difficult and expensive for thieves to turn dumps into cold hard cash. This same increase in card-not-present fraud has occurred in virtually every other country that long ago made the chip card transition, including Australia, Canada, France and the United Kingdom.

The increasing value of CVV data may help explain why we’ve seen such a huge uptick over the past year in e-commerce sites getting hacked. In a typical online retailer intrusion, the attackers will use vulnerabilities in content management systems, shopping cart software, or third-party hosted scripts to upload malicious code that snarfs customer payment details directly from the site before it can be encrypted and sent to card processors. Continue reading

And yet, here I am again writing the second story this week about a possibly serious security breach at an Indian company that provides IT support and outsourcing for a ridiculous number of major U.S. corporations (spoiler alert: the second half of this story actually contains quite a bit of news about the breach investigation).

And yet, here I am again writing the second story this week about a possibly serious security breach at an Indian company that provides IT support and outsourcing for a ridiculous number of major U.S. corporations (spoiler alert: the second half of this story actually contains quite a bit of news about the breach investigation).

According to security firm

According to security firm  Adobe’s Patch Tuesday includes security updates for its

Adobe’s Patch Tuesday includes security updates for its